- Contents

The FIFA World Cup 2026 kicks off this summer across the United States, Canada, and Mexico, the first edition to feature 48 teams and the largest in the tournament’s history. For Africa, the stakes are especially high: ten African nations have qualified, the most the continent has ever sent to a single World Cup.

This study mirrors our 2022 FIFA World Cup report, which tracked African sentiment and viewing behaviour during the last tournament. GeoPoll surveyed 3,274 people across Kenya, Ghana, Nigeria, South Africa, Uganda, Cameroon, and Egypt in June 2026, to capture how the continent is experiencing this moment, from viewing habits and team loyalties to betting behaviour and broadcast awareness.

Key Findings

- Near-universal intent to watch the 2026 World Cup: An average of 94% of respondents across the seven countries say they plan to watch or follow the tournament, peaking at 97% in South Africa and 96% in Ghana.

- Strong general football interest across markets: Average interest ranges from 7.3/10 in Cameroon to 8.0/10 in Egypt, showing consistently high baseline engagement with the sport across all countries surveyed.

- Television remains dominant but multi-platform viewing is rising: 79% plan to watch on TV, while 62% will use mobile phones, 39% free online streaming, and 34% social media platforms—highlighting increasingly fragmented consumption habits.

- High level of sports betting engagement: 52% of respondents have placed a football bet in the past 12 months, rising to 64% in Kenya, 60% in Ghana, and 58% in South Africa, but dropping to 25% in Egypt.

- Football is highly social, with home viewing dominant: 73% plan to watch from home, while 9% will watch in pubs/restaurants and 19% engage in betting during matches, showing football as both a private and social experience.

- Europe dominates World Cup winner predictions: France leads at 19%, followed by Spain (14%), Portugal (12%), with Brazil (9%) and Argentina (8%) trailing; in Africa, local optimism remains strong, including 81 Egyptian respondents predicting Egypt will win.

Passion for the game

Football is more than a pastime in the seven countries surveyed, it is a significant part of daily life. Ahead of the 2026 FIFA World Cup, GeoPoll asked respondents to rate their interest in football and in the World Cup on a scale of 1 to 10. Interest in football is consistently high, ranging from 7.3 in Cameroon to 8.0 in Egypt, highlighting the sport’s widespread appeal across the continent. Egypt’s strong score reflects the country’s deep football culture, fueled by club competitions, continental tournaments, and national team ambitions.

Interest in the 2026 World Cup is even higher in most markets, with South Africa and Egypt leading at 8.4, followed by Ghana (8.2), Uganda (8.0), and Kenya (7.9). Cameroon is the only country where World Cup interest (7.2) is slightly lower than general football interest, likely due to the Indomitable Lions not qualifying for the tournament. Even so, the findings show that football remains deeply embedded in the lives of fans across all seven countries.

One theme stands out clearly: the World Cup lifts interest beyond its everyday level. Fans who might describe themselves as casual football followers during the domestic club season become fully engaged when the global tournament arrives. This tournament-driven uplift is consistent across demographics and geographies, and it has direct implications for brands, broadcasters, and advertisers looking to reach African audiences at peak attention.

Intent to Watch the 2026 World Cup Across Africa

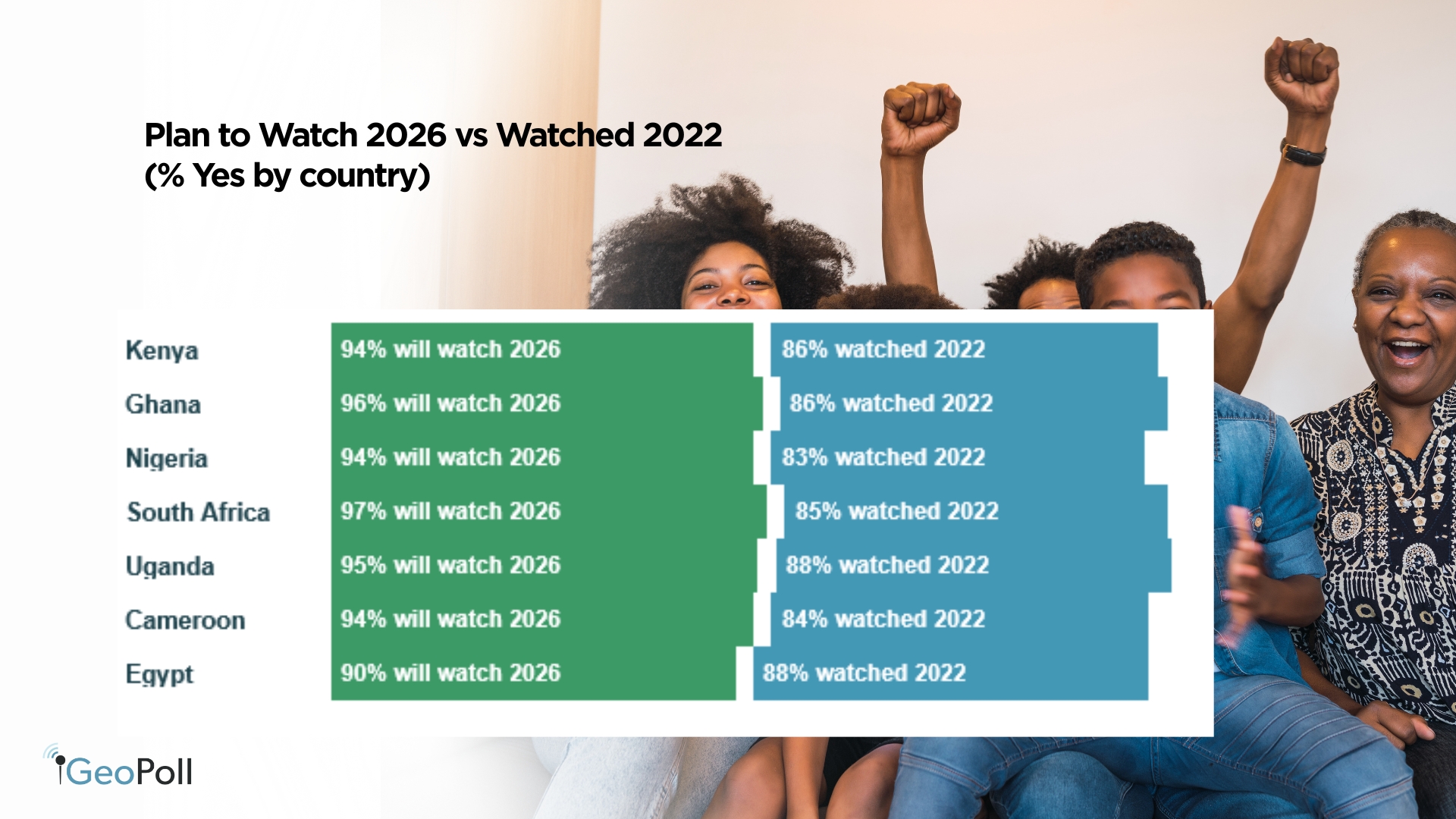

Perhaps the most striking finding in this survey is the near-universal intent to watch or follow the 2026 FIFA World Cup. Across the seven countries, an average of 94% of respondents say they plan to engage with the tournament in some form. This peaks at 97% in South Africa and 96% in Ghana, while Egypt records 90% still exceptionally high, yet the lowest in the sample.

These figures reflect a broad-based cultural phenomenon rather than a narrow or urban-centred interest. GeoPoll’s methodology captures respondents across urban, peri-urban, and rural areas, as well as across gender and income groups, underscoring the depth of national-level engagement with the tournament. When compared with actual viewership from the 2022 World Cup in Qatar, where 85% of respondents reported watching matches, the 2026 intent figures suggest growing enthusiasm rather than saturation. Uganda stands out with 88% reported viewership in 2022, rising to a projected 95% intent for 2026, reinforcing the upward trajectory in World Cup engagement across the continent.

How Fans Across Africa Will Follow the 2026 World Cup

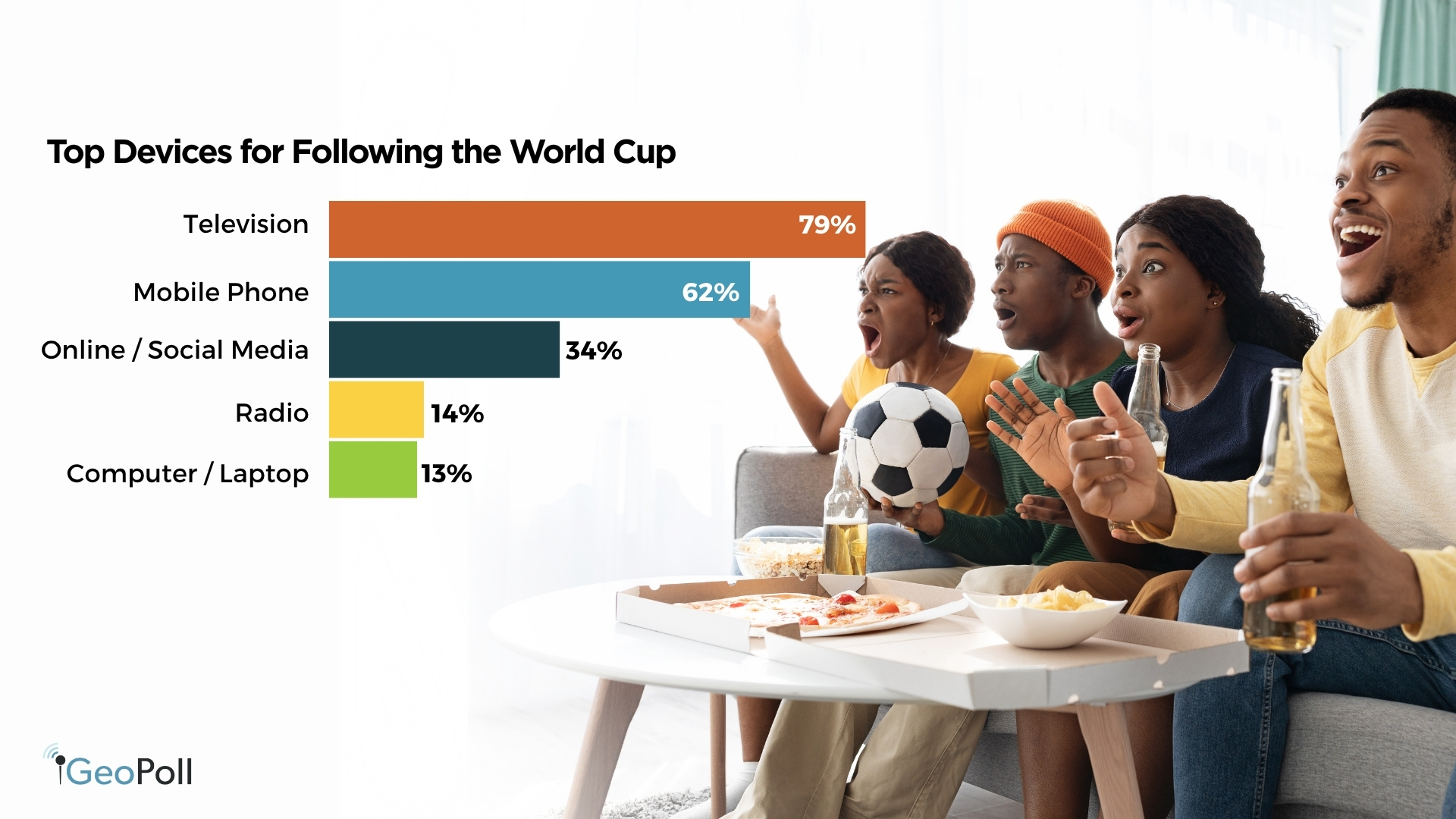

Television remains the dominant way of following the World Cup across the continent, with 79% of respondents saying they plan to watch matches on a TV set. This underscores the continued strength of broadcast and pay-TV infrastructure in most markets. However, mobile phones are quickly becoming a major companion screen, with 62% of respondents planning to follow matches on their devices. In Nigeria, this shift is already more advanced, with 66% of respondents citing mobile phones as their primary viewing device, reflecting the rapid expansion of affordable smartphones and mobile data, particularly among younger and lower-income groups.

Digital and social platforms are also playing an increasingly important role. Around 34% of respondents plan to follow the tournament via online streams and social media channels such as YouTube, WhatsApp, and X (formerly Twitter), with Kenya leading in this category due to strong mobile internet penetration and highly engaged digital audiences. Meanwhile, radio remains a key access point for 14% of respondents, particularly in markets such as Uganda and Cameroon, where it continues to provide an essential and widely accessible form of live football coverage.

Paid vs Free and the Streaming Question

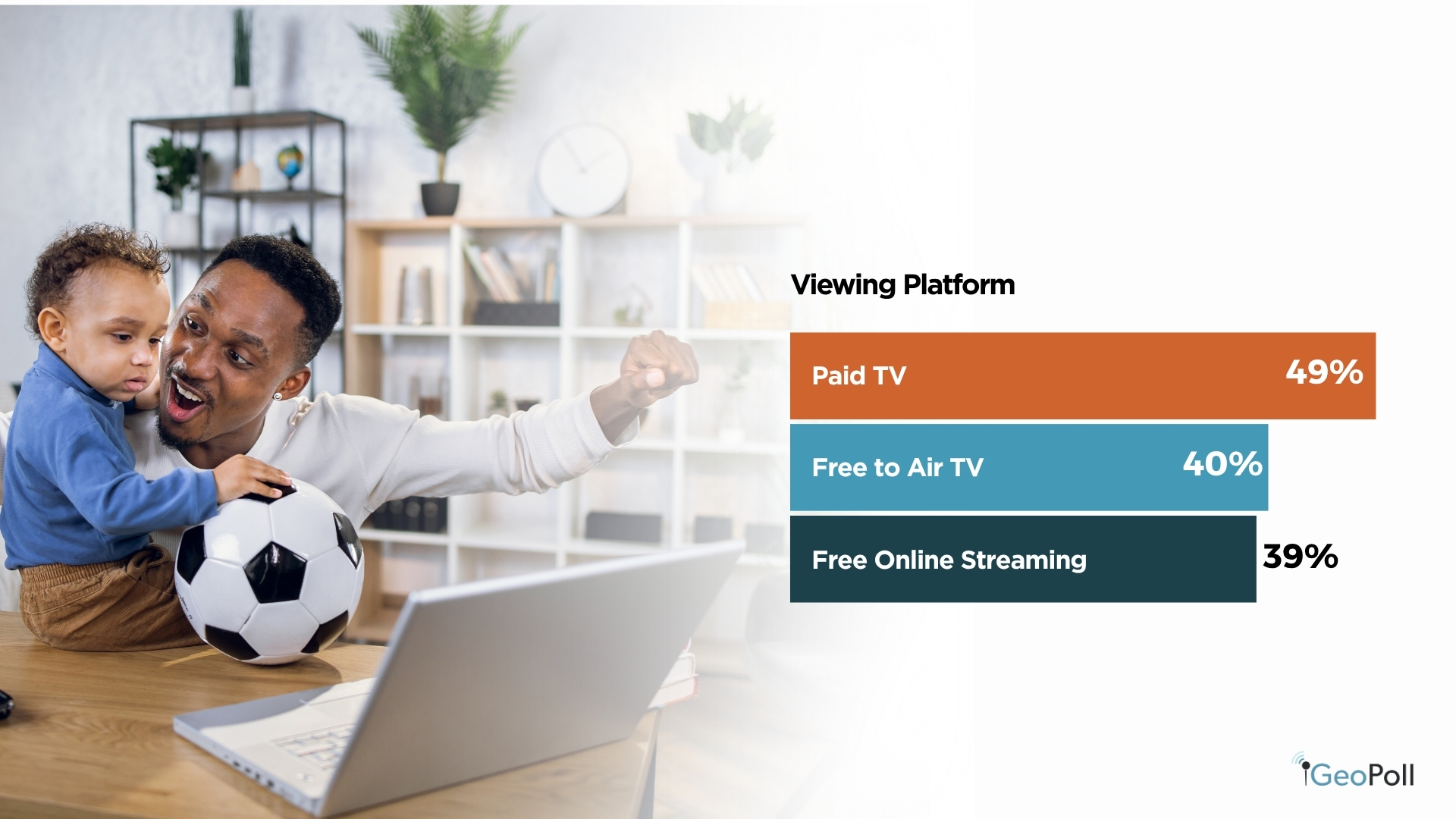

When it comes to platforms for accessing live coverage, the picture across the seven countries is more evenly split than device usage alone might suggest. Paid TV leads with 49%, followed closely by free-to-air television at 40%, free online streaming at 39%, and paid online streaming at 33%. This distribution highlights a nuanced reality: Africa is not a single, uniform media market, but a patchwork of differing access models and viewing behaviours.

Country-level differences further reinforce this diversity. South Africa stands out with a strong reliance on paid TV (66%), reflecting its established satellite and subscription ecosystem, while Cameroon and Ghana lean more heavily on free-to-air broadcasts, making FTA rights critical for reaching mass audiences in those markets. The near parity between free-to-air TV and free online streaming is particularly notable, signalling the growing importance of digital access. A substantial segment of viewers, especially younger, urban audiences, already turn to online platforms for live football, whether ad-supported or unofficial. For rights holders and broadcasters alike, the implication is clear: reaching audiences effectively requires a multi-platform approach that mirrors how fans already consume content.

Nigeria is the most mobile-first viewing market in the survey. 66% of Nigerian respondents will follow the World Cup on their phone; compared to 45% in South Africa, where paid TV is dominant.

Home Remains the Center of World Cup Viewing

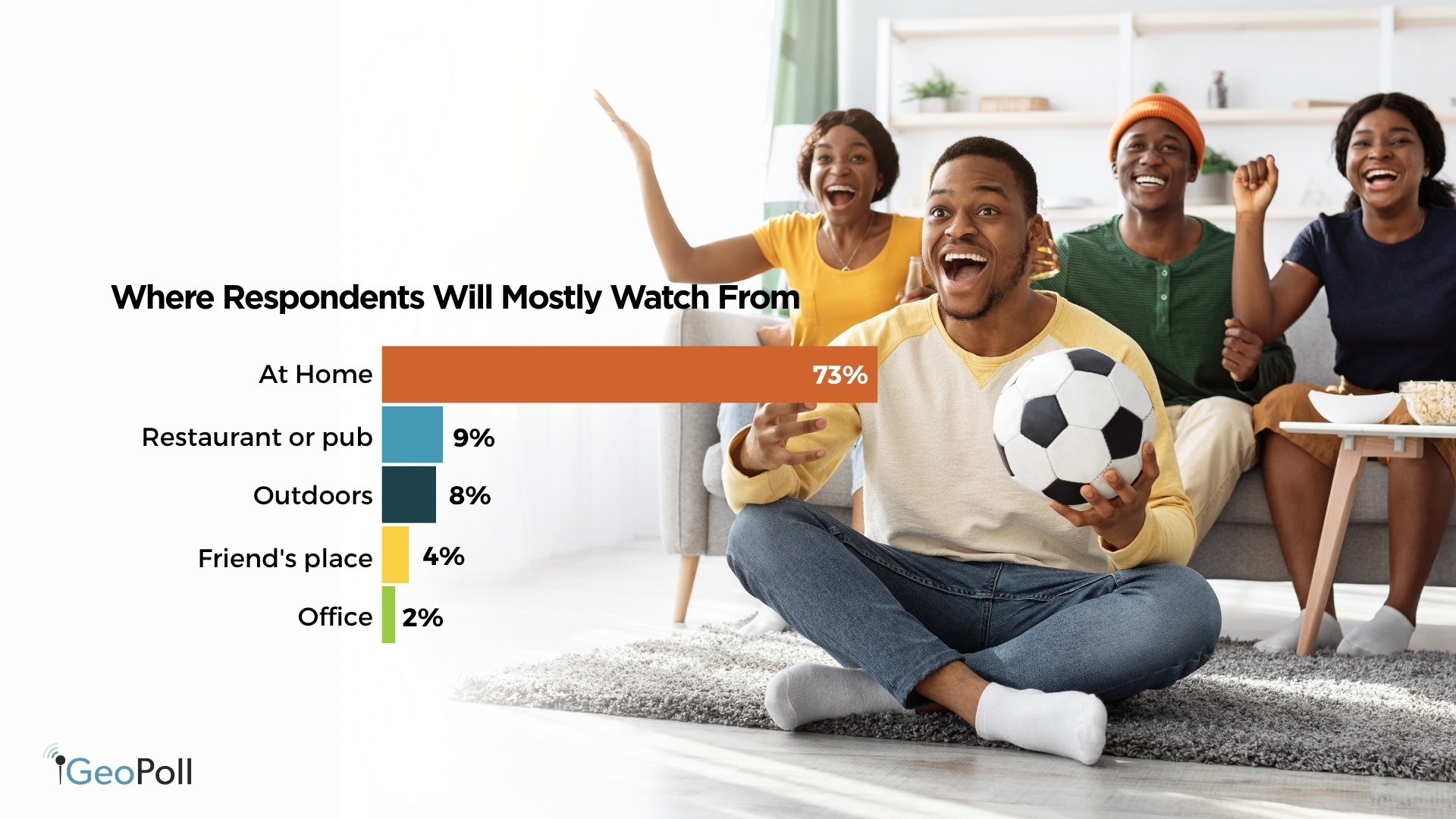

Home viewing overwhelmingly dominates across all seven countries surveyed, with 73% of respondents saying they plan to watch the 2026 World Cup from home. However, the remaining quarter of viewers reveals important insights into how football functions as a shared social experience across the continent.

Restaurants and pubs account for 9% of viewing overall, underscoring the role of public venues as key gathering points for major matches. This is especially pronounced in Nigeria, where communal viewing in commercial spaces is a well-established matchday tradition. Ghana records the highest rate of outdoor and public-space viewing at 9%, reflecting the popularity of large-screen setups in urban centres where football is often experienced collectively. Workplace viewing remains limited at 2% overall, but still present across markets, an understated reminder that during key kick-off times, productivity across some offices may quietly compete with matchday excitement.

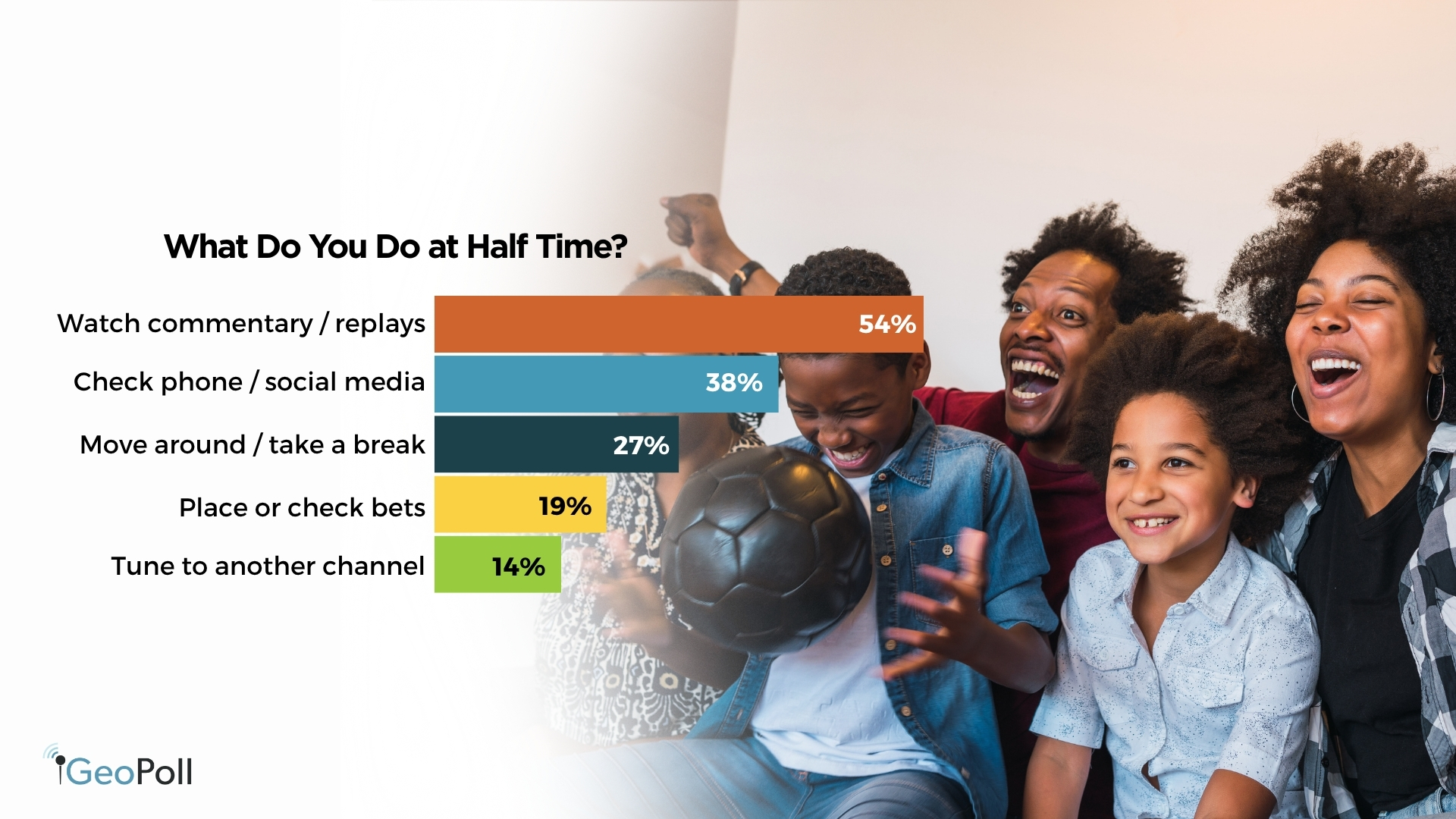

Half-Time as a Window into Fan Behaviour

Half-time offers a revealing snapshot of viewing behaviour beyond the 90 minutes of play. Across all countries, the most common activity is remaining engaged with match commentary and replays (54%), showing that for many fans, the break is not a pause in attention but an extension of the viewing experience. Close behind, 38% of respondents say they turn to their mobile phones—checking scores, sharing reactions, following analysis, or scrolling through social media for highlights and real-time commentary.

Betting activity is also a notable part of the half-time experience. One in five respondents (19%) report placing or reviewing bets during the interval, rising to 27% in Kenya and 19% in South Africa, where in-play and half-time betting markets are more actively integrated into the viewing ecosystem. This reinforces the growing convergence between football consumption and sports betting, where watching and wagering increasingly operate as part of a single, continuous experience.

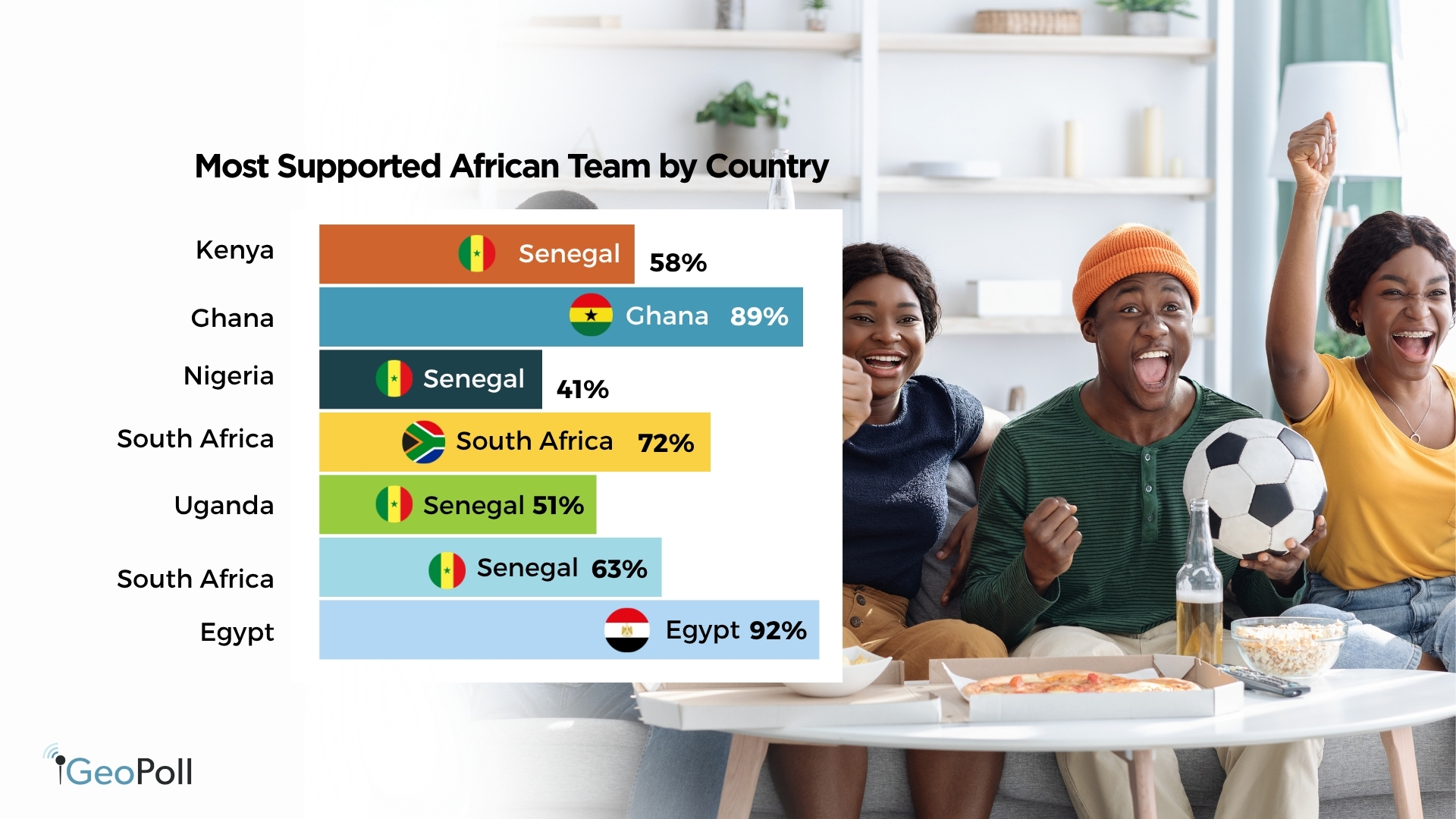

African Team Allegiances Point to Strong Home Pride

With 10 African nations qualifying for the 2026 FIFA World Cup, continental team allegiance emerges as one of the most revealing dimensions of the survey. GeoPoll asked respondents which African teams they are supporting, uncovering a mix of strong national loyalty and broader pan-African solidarity.

Home-country support is dominant where teams have qualified. Egypt records the highest level of domestic backing, with 92% of respondents supporting the Pharaohs, followed closely by Ghana at 89%, reflecting deep national pride and emotional investment in their teams’ return to the global stage. South Africa’s Bafana Bafana attract support from 72% of respondents, a solid but comparatively lower figure that reflects a more diversified national sports landscape where football shares attention with rugby and cricket.

In countries without a qualified team, support shifts decisively toward regional favourites. Senegal emerges as the continent’s default second team, leading in Kenya (58%), Cameroon (63%), and Uganda (51%), while also holding strong appeal in Nigeria (41%). Morocco also enjoys widespread admiration, consistently ranking among the top choices across non-qualifying countries, with 38% support in Nigeria alone. Senegal’s prominence is closely linked to its status as reigning Africa Cup of Nations champions and its roster of globally recognised players, while Morocco’s continued popularity builds on its historic 2022 World Cup semi-final run. Together, the two teams dominate the pan-African imagination, shaping a shared continental rooting interest beyond national borders.

Senegal is Africa’s adopted team. In every country without a side of its own in the tournament, Senegal is the most supported African nation — a continent rallying behind the Lions of Teranga.

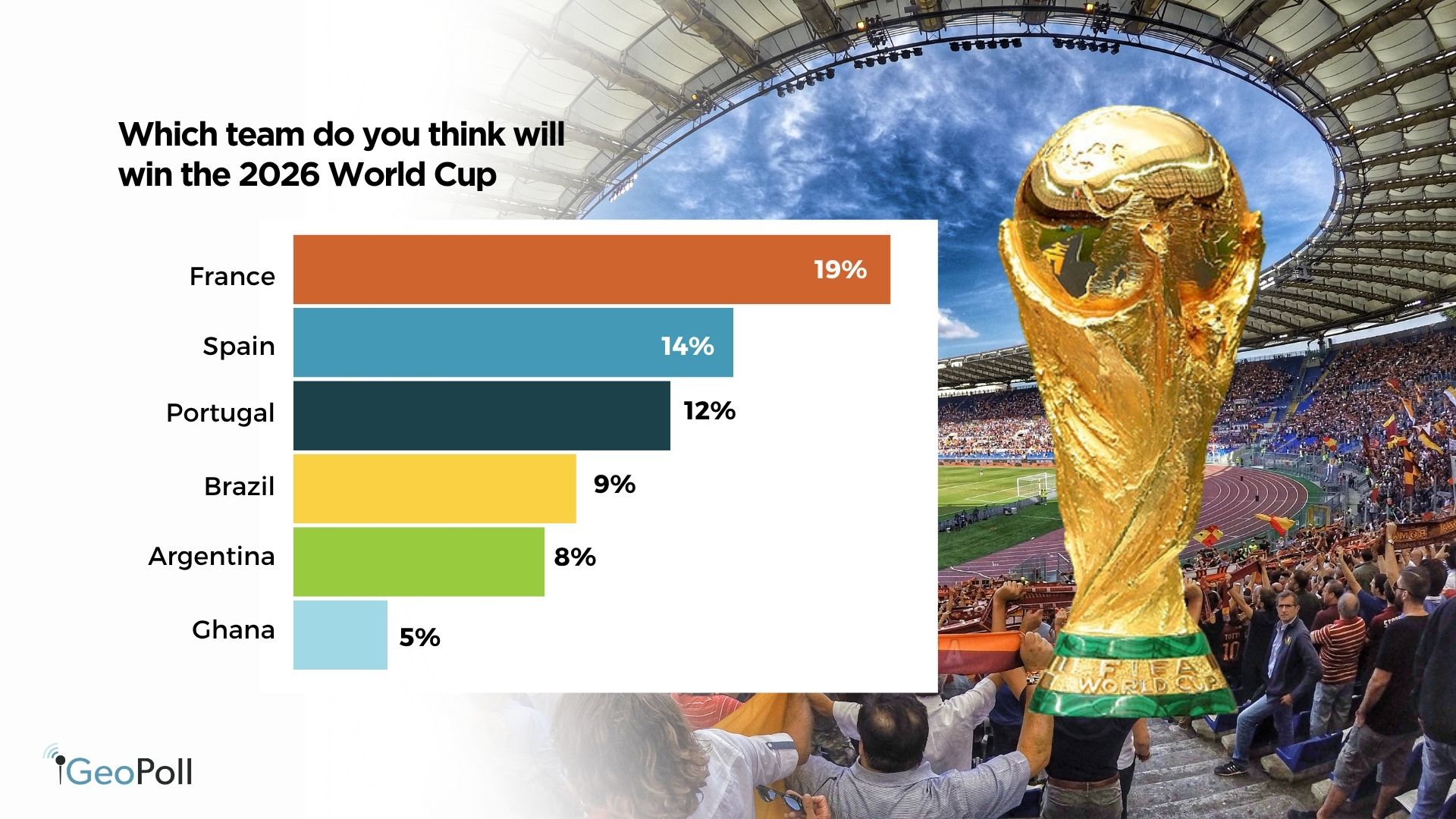

Who Do Respondents Think Will Win the Tournament?

There is a clear distinction between who fans support and who they believe will actually win the 2026 FIFA World Cup. When asked to predict the eventual champion, a measure of football judgement rather than emotional loyalty, respondents overwhelmingly point to European teams as the most likely winners.

France leads the overall predictions at 19%, followed by Spain at 14% and Portugal at 12%. Brazil (9%) and Argentina (8%) remain the strongest South American contenders, but the balance of expectation firmly tilts toward Europe. France’s dominance is shaped not only by its recent football pedigree, including the 2018 World Cup triumph, but also by the strong visibility of players of African heritage such as Kylian Mbappé, Eduardo Camavinga, and Ibrahima Konaté, who resonate deeply with African audiences.

In Kenya, Uganda, and Cameroon, France is the most commonly predicted winner, while Nigeria leans toward Portugal, likely influenced by the global stature of Cristiano Ronaldo. Egypt stands out for its strong home optimism, with 81 respondents predicting Egypt will lift the trophy, an expression of national pride that persists even against global consensus.

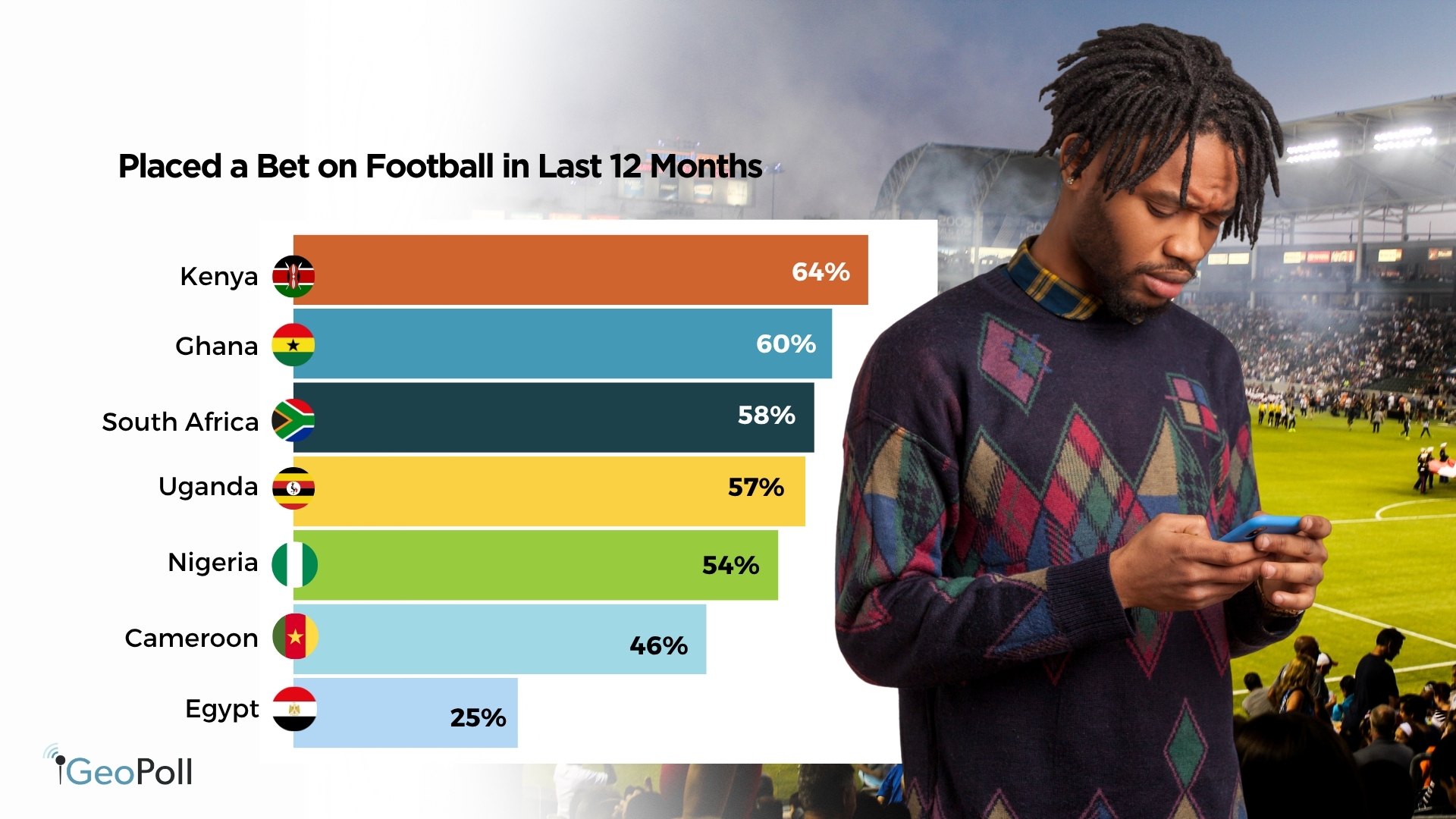

Sports Betting is Now Embedded in Football Culture Across Africa

Sports betting in Africa has expanded rapidly over the past decade, driven by rising smartphone penetration, aggressive operator marketing, and a young, mobile-first population deeply engaged with sport. The FIFA World Cup stands out as one of the most important moments in the sports betting calendar, and the data from this survey confirms just how embedded betting has become in the football-watching experience across several key markets.

Overall, 52% of respondents say they have placed a bet on football in the past 12 months, underscoring that this is no longer a marginal activity but a mainstream form of engagement with the game. Kenya leads at 64%, reflecting a highly developed betting ecosystem. Ghana (60%), South Africa (58%), Uganda (57%), and Nigeria (54%) also report high participation, all pointing to a strong regional integration between football fandom and wagering.

Egypt stands as a clear outlier at 25%, the lowest rate in the survey by a wide margin. This is shaped by a different regulatory and cultural environment, where gambling is heavily restricted and lacks the same app-driven normalisation seen in other markets.

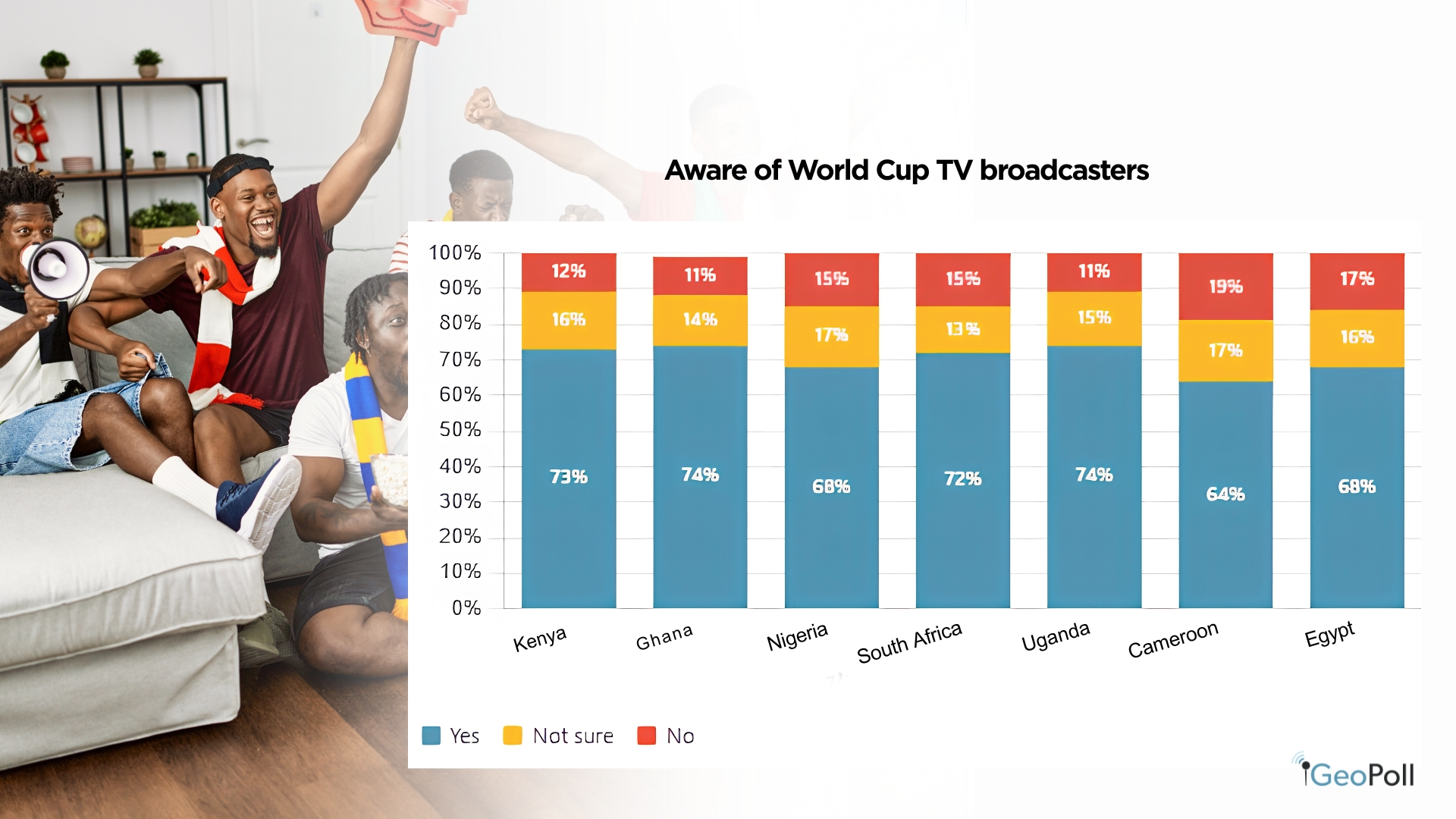

Aware of World Cup TV broadcasters

GeoPoll measured broadcast awareness by asking respondents whether they know which channels in their country will show live FIFA World Cup matches. Across the seven countries, 74% of respondents said they know where to watch, indicating a solid majority—but also leaving 26% who are either unsure or unaware. For broadcasters and rights holders, this gap represents both a communication challenge and a clear opportunity to convert interest into confirmed viewership.

Awareness levels are relatively consistent across most markets, with Ghana and Uganda leading at 74%, followed closely by Kenya at 73% and South Africa at 72%. These are markets where broadcast rights are typically well publicised and where dominant pay-TV platforms help centralise messaging around a single access point. Cameroon stands out at the lower end, with 64% awareness, likely reflecting reduced urgency in the absence of its national team in the tournament, which diminishes the immediate incentive for fans to track broadcast details.

The remaining “not sure” group is particularly significant. In Egypt, 16% of respondents fall into this category despite the country’s high levels of football interest overall. This suggests a highly engaged audience that is still undecided on access details rather than disengaged from the tournament itself.

World Cup Brand Promotions Awareness

Brand associations with 2026 World Cup promotions are strongly concentrated among a few global players, with Coca-Cola dominating at 31%, more than double its nearest competitor. Adidas follows at 14%, while Nike ranks third at 8%, indicating that traditional sportswear giants remain highly visible but significantly behind the soft drinks category leader. Pepsi (5%) sits further back, alongside smaller shares for Hisense and Visa at 3% each, and DStv and MTN at 2% apiece. Overall, the results highlight the continued dominance of legacy global sponsors in shaping World Cup marketing recall, with Coca-Cola in a particularly powerful position across all markets.

Methodology/About this Survey

This exclusive survey was powered by GeoPoll’s AI platform; Tuucho run via the GeoPoll mobile application and WhatsApp in Kenya, Ghana, Nigeria, South Africa, Uganda, Cameroon, and Egypt in early June 2026 the sample size was 3,274, composed of random users between 18 and 50. Since the survey was randomly distributed to an and the results are slightly skewed towards younger respondents. All questions were self-administered via mobile survey in English, French and Arabic.

The findings show that football in the surveyed African markets is characterised by exceptionally high engagement, near-universal intent to watch the 2026 World Cup, and deeply embedded viewing habits that span TV, mobile, and social platforms. While television remains dominant, digital and mobile consumption is rising quickly, reflecting a shift toward more fragmented and multi-platform access. Betting is also a major feature of the football ecosystem, with over half of respondents having placed a bet in the past year and in-play wagering forming part of the matchday experience for many. At the same time, fandom extends beyond national borders, with strong support for both home teams and leading continental sides such as Senegal and Morocco. Together, these dynamics point to a highly engaged, digitally evolving, and commercially active football audience across Africa ahead of the 2026 World Cup.

Please get in touch with us to get more details about our capabilities, explore more on various topics in Africa, Asia, and Latin America.