In early May 2026, GeoPoll surveyed 1,120 Kenyan adults to understand how the country’s ongoing fuel shortage is being felt on the ground. The picture that emerged is one of nearuniversal disruption. Across every dimension we measured transport, household finances, business operations, and public outlook, the shortage has left a visible mark on daily life.

The study was conducted by GeoPoll using its WhatsApp-based data collection mode and end-user mobile app across Kenya between May 6 and 9, 2026. A total of 1,120 respondents participated, providing insights into public awareness and lived experiences of the ongoing fuel shortage in the country.

The study explored key themes including awareness of the shortage, personal and household experiences, daily disruptions, economic effects, coping strategies, perceptions of government response, and expectations for the future.

At a glance

- Awareness of the ongoing fuel shortage in Kenya is very high, with 96% of respondents reporting that they are aware of the situation.

- A significant majority of respondents, 81%, reported having personally experienced difficulty accessing fuel in the past two weeks in Kenya.

- A large majority of respondents, 94%, reported that their household expenses have increased as a result of the fuel shortage in Kenya. Notably, more than half of this group (53%) indicated that the increase has been significant, highlighting the strong financial pressure placed on households.

- Among public transport users, 96% reported an increase in fares in Kenya, with 51% stating that the increase has been significant.

- A notable portion of respondents, 30%, attribute the ongoing fuel shortage in Kenya to geopolitical tensions.

- A slight majority of respondents, 53%, expect the fuel shortage in Kenya to persist for more than a month or potentially develop into a longer-term issue.

Awareness and Personal Experience

Crisis events often reach a point where they move beyond media coverage and become part of everyday lived experience. In the case of the fuel shortage in Kenya, this transition appears to have fully occurred. Awareness is near-universal at 96%, indicating that the issue is widely recognized across the population.

However, awareness alone does not capture the full extent of the situation. The more important indicator is how deeply the shortage is affecting daily routines, and the data shows clear evidence of widespread disruption across mobility, household spending, and transport costs.

A total of 81% of respondents reported having personally experienced difficulties accessing fuel in the past two weeks in Kenya. This indicates that a large majority of those surveyed are not only aware of the situation, but are directly affected by it in their day-to-day lives. Many have faced long queues at petrol stations, been unable to refuel when needed, incurred higher-than-expected costs, or had to adjust their routines due to inconsistent fuel availability.

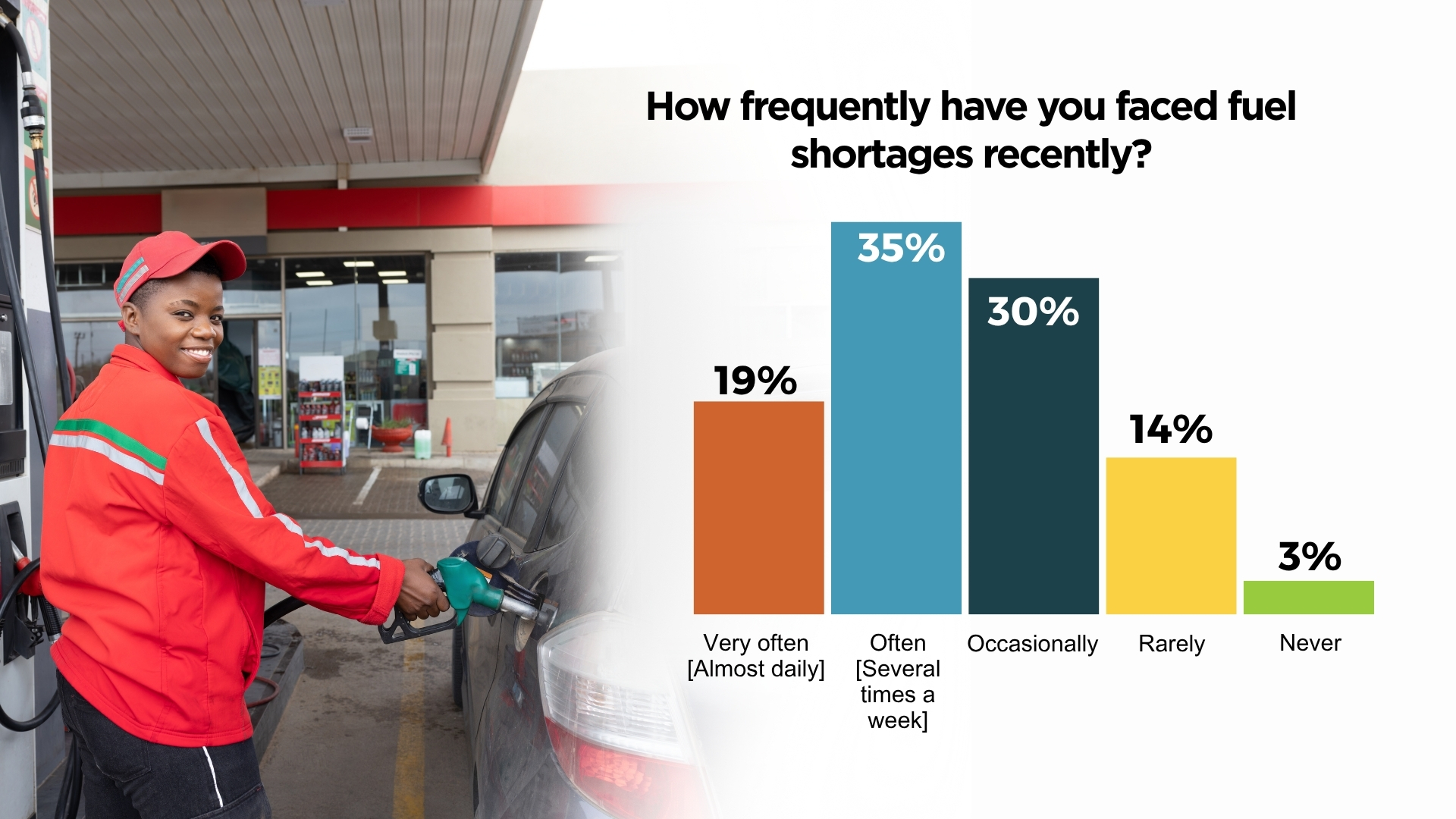

More than half of respondents (53%) reported that they experienced fuel shortages very often or on multiple occasions each week in Kenya. This indicated that the issue was not occasional, but a recurring disruption that had become part of daily routines for many people, affecting how they moved, worked, and planned their activities.

Only 3% reported that they had never experienced a fuel shortage, highlighting how widespread and persistent the challenge had been across the surveyed population.

The Cost of Getting Around

Kenya is a country constantly in motion, where millions of people rely on public transport each day, including matatus, boda bodas, and tuk-tuks, to get to work, school, markets, and health facilities. When fuel becomes scarce or costly, the impact is not confined to petrol stations; it moves with every journey, affecting passengers, goods, and services across the transport network.

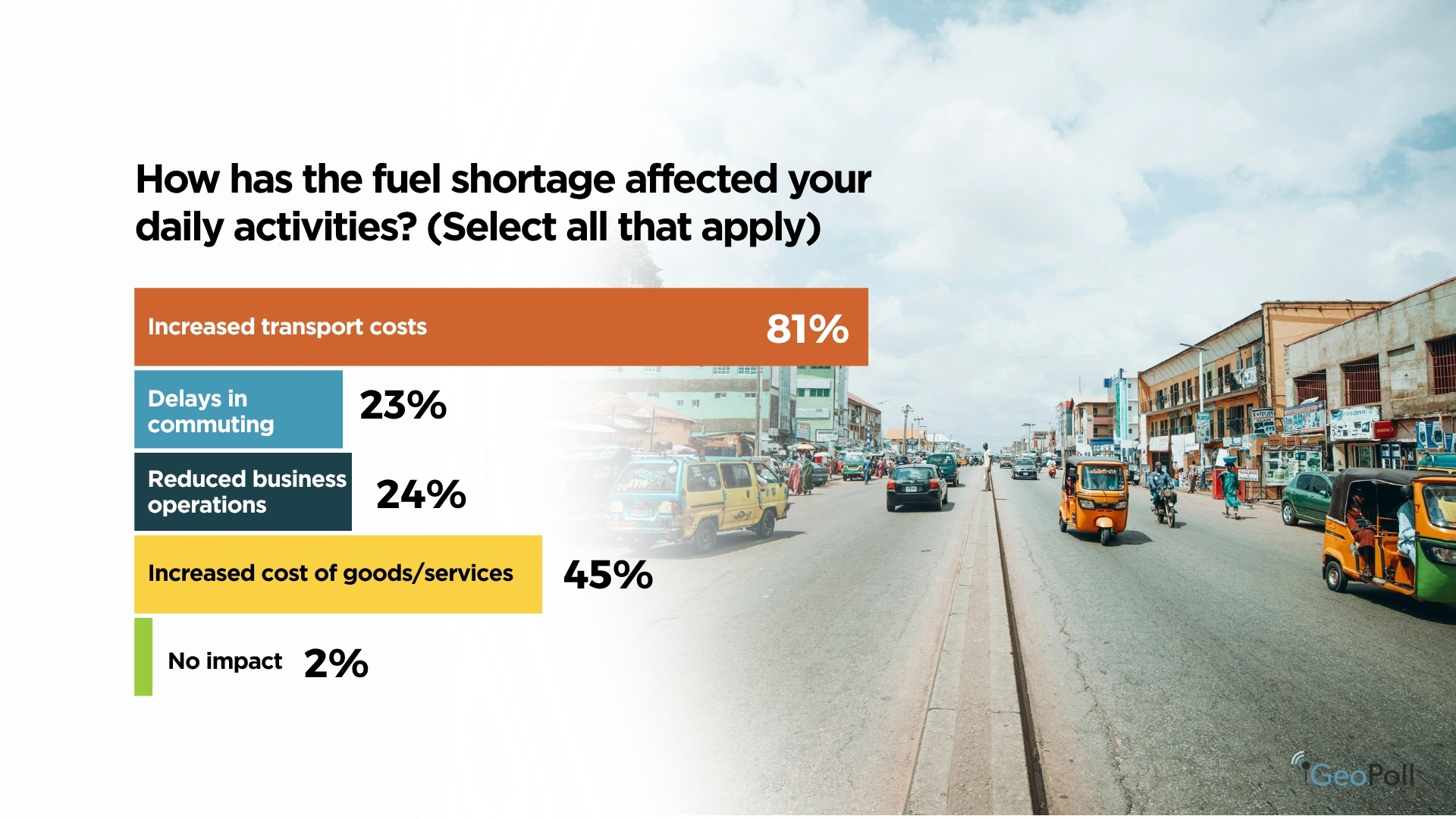

The data clearly reflect this reality. Increased transport costs emerged as the most widely reported impact of the fuel shortage, cited by 81% of respondents.

Impact on Daily Activities

Respondents were asked to select all ways in which the fuel shortage had affected their daily lives. Beyond transport, 45% reported an increase in the cost of goods and services, reflecting the ripple effects of higher logistics and delivery expenses across the supply chain. A quarter (25%) indicated reduced business operations, while 23% experienced commuting delays that disrupted their daily schedules.

Overall, the findings pointed to widespread disruption across everyday economic activity, where most forms of movement and service delivery had become more costly or difficult. Only 2% of respondents reported that the shortage had not affected their daily life.

What Happened to Transport Fares?

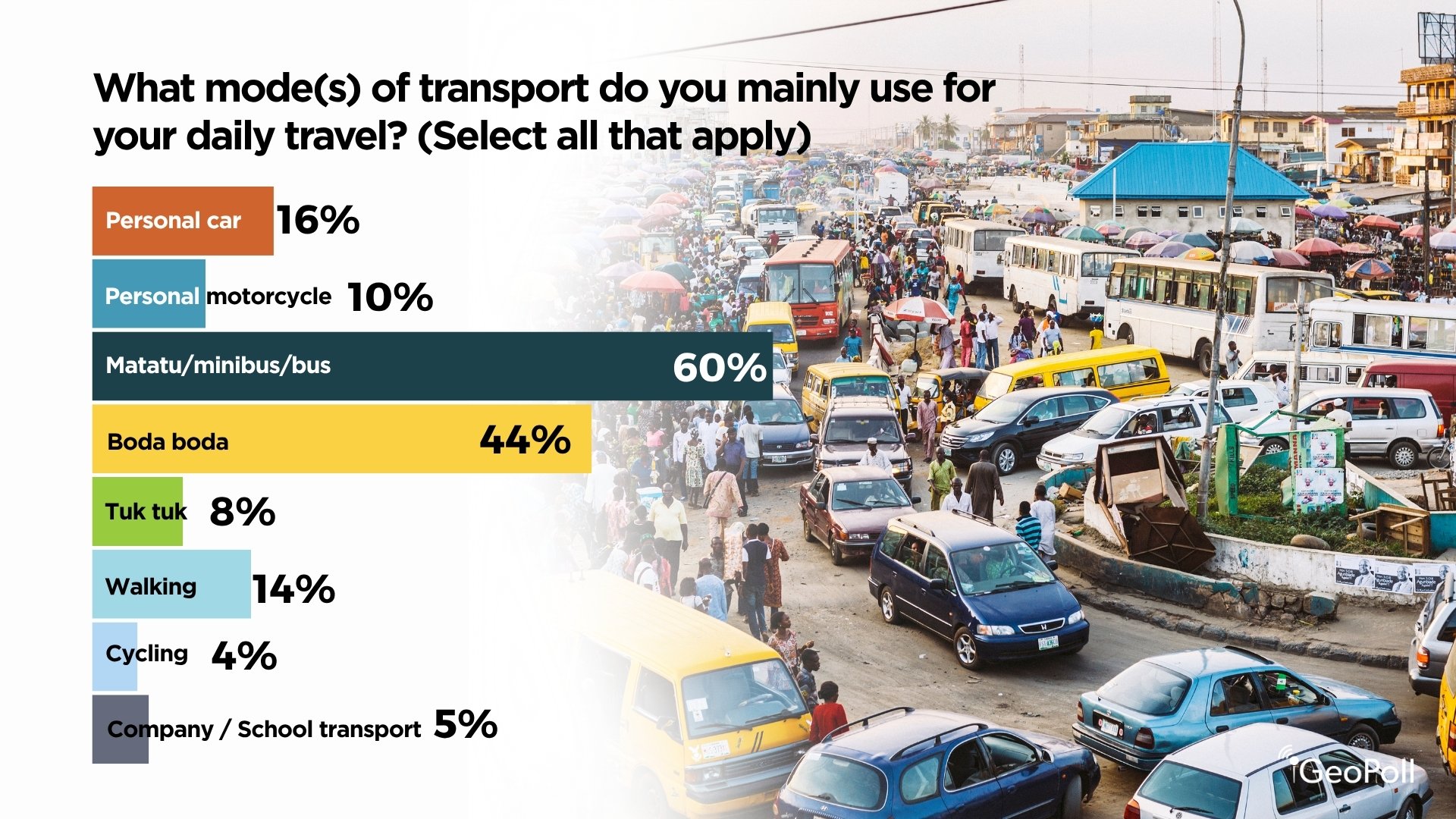

More than half, 60% of respondents reported relying primarily on matatus or buses for their daily travel, while 44% used boda bodas. These modes of transport are not occasional alternatives, they form the core of daily mobility for most people. As fuel costs rise, operators typically pass these increases on to passengers, leaving limited alternatives for commuters.

The impact on fares was near-universal. A total of 96% of public transport users reported an increase in fares, with 51% describing the rise as significant. A further 45% noted that fares had increased, though less sharply. Only a small minority, less than 4%, reported no change in transport costs.

96% of public transport users say fares have gone up. Almost no one has been spared.

Household Finances Under Pressure

The combined effect of higher transport costs and rising prices for goods has been clearly reflected in household budgets. When respondents were asked about the overall impact of the fuel shortage on their household expenses, the responses were overwhelmingly consistent.

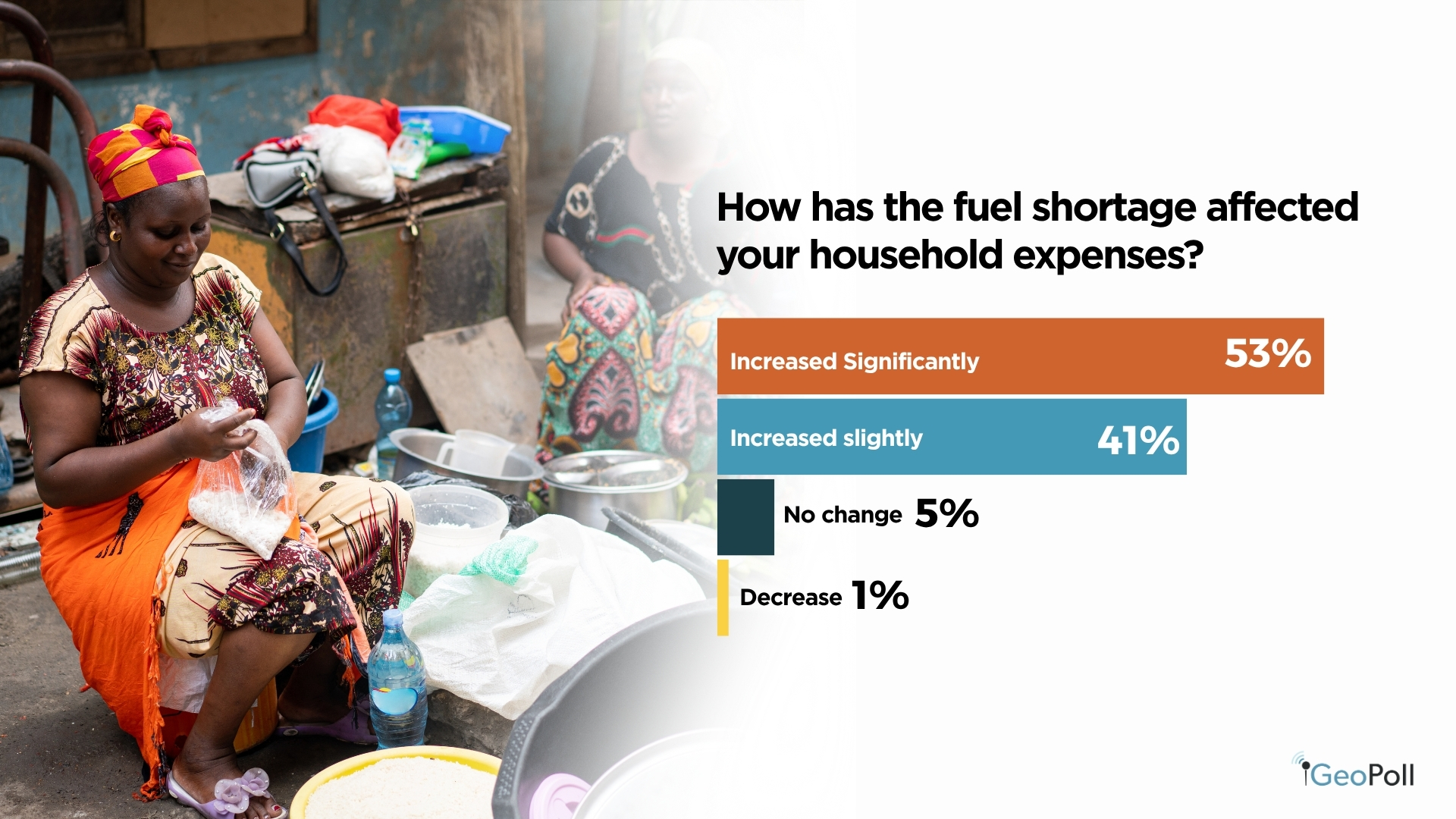

A total of 94% reported that their household expenses had increased. More than half of these respondents (53%) described the increase as significant rather than marginal. This points to a shift from manageable cost adjustments to more pronounced financial pressure for many households. Only 5% reported no change in their expenses, while just 1% indicated a decrease.

For households already operating under constrained budgets, even moderate increases in daily costs translate into reduced financial flexibility. The breadth of the response suggests that the impact has been widely felt across different segments of the population.

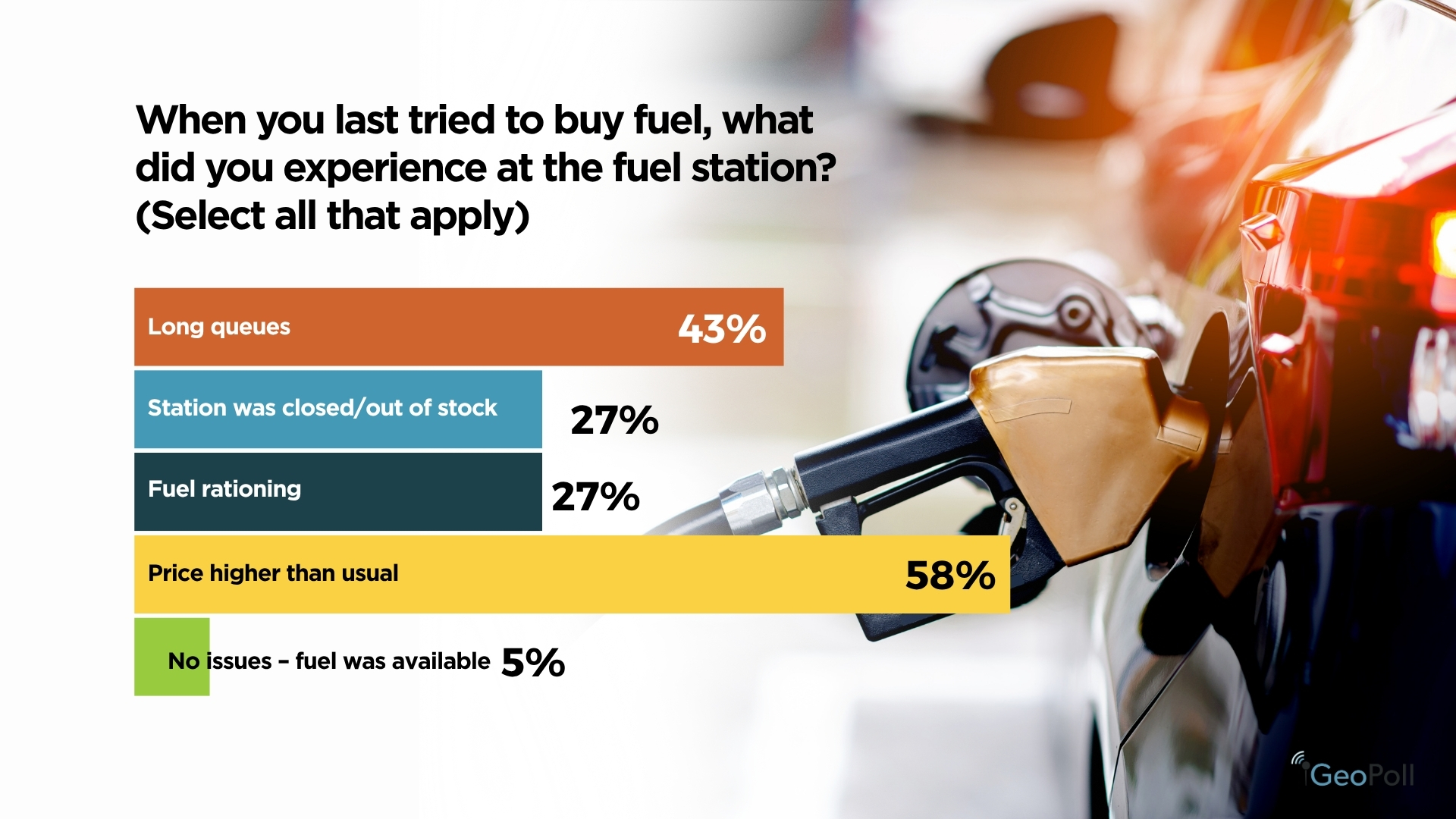

The View From the Petrol Station

Among the 195 respondents who had recently attempted to purchase fuel directly, either for their own vehicle or one they were travelling in, very few described the experience as smooth. Only 5% reported finding fuel available without any challenges, while the vast majority encountered at least one difficulty at the station.

The most commonly reported issue was higher-than-expected prices, cited by 58% of respondents. In addition, 43% experienced long queues at fuel stations, indicating sustained pressure on available supply. More than a quarter (27%) found stations closed or completely out of stock, while another 27% reported experiencing fuel rationing, where purchases were limited to restricted quantities.

Taken together, these findings point to a supply situation that extended beyond price increases alone. The combination of higher prices, long waiting times, stock shortages, and rationing reflected significant strain in fuel availability during the survey period, with uninterrupted access reported by only a small minority.

“One in four fuel buyers found the station closed or out of stock. One in four more were rationed.”

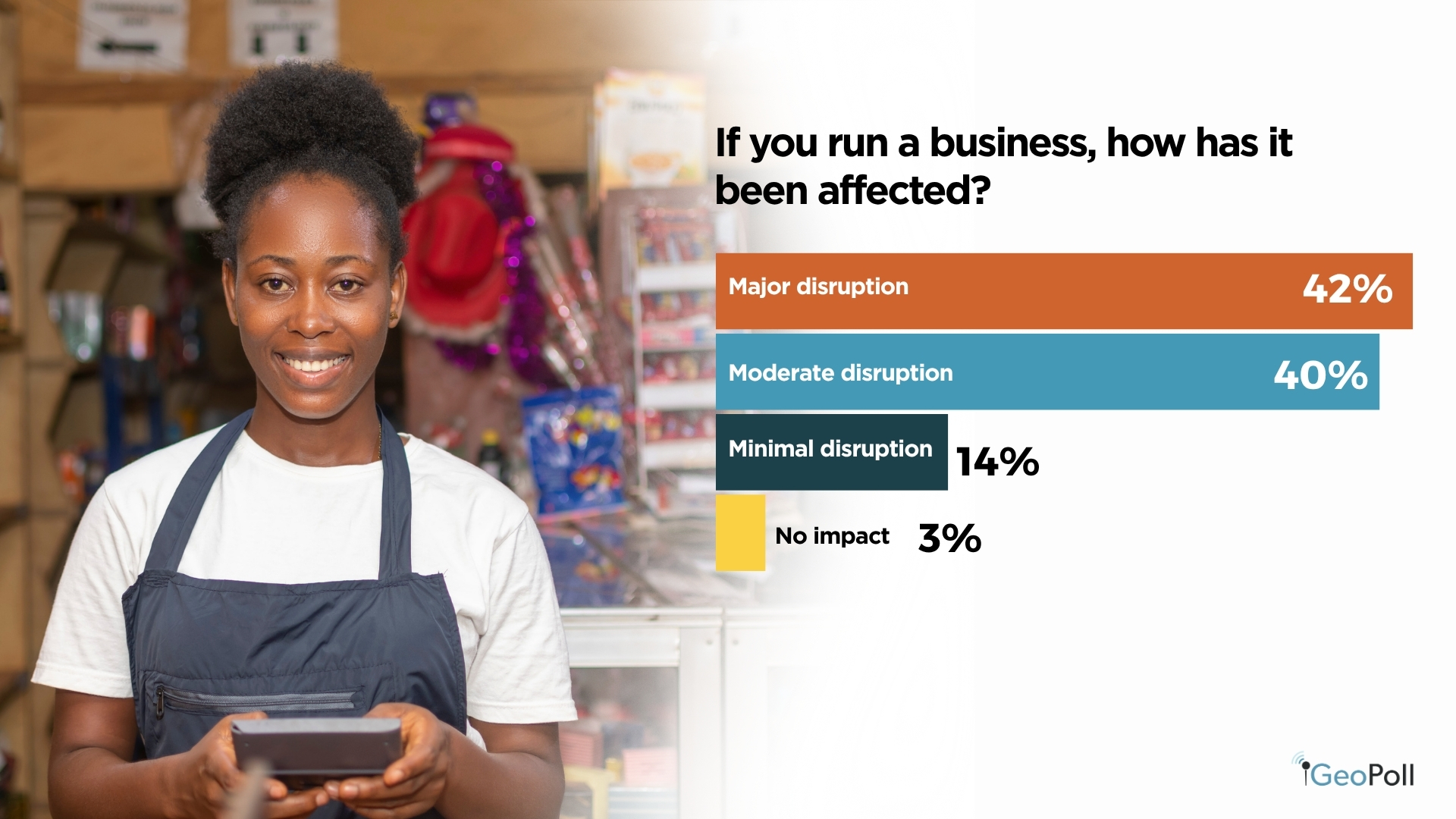

Businesses on the Back Foot

Among the 904 respondents in this group, only 3% reported that their business operations had not been affected by the fuel shortage. The remaining 97% experienced some level of disruption, ranging from minor challenges to severe operational difficulties.

A significant share, 42%, described the impact on their business as major, pointing to widespread strain on day-to-day operations. These disruptions likely included increased operating costs, delayed deliveries, reduced customer activity, slower transport and logistics, and interruptions to normal business schedules. An additional 40% reported moderate disruption, showing that the effects of the shortage were being felt across a broad range of businesses and economic activities.

82% of business operators report major or moderate disruption. Just 3% say they have not been affected.

How Kenyans Are Adapting

Respondents reported adopting a range of coping strategies in response to the fuel shortage and rising transport costs. The most common adjustment was walking or cycling, cited by 40% of respondents. For many, this reflected a practical response to reduced transport affordability or availability, often requiring longer travel times and added physical strain in daily routines.

A further 39% reported reducing non-essential travel, indicating that many households were limiting discretionary movement in order to manage costs. Meanwhile, 30% said they were relying more heavily on public transport, despite widespread reports of increased fares.

Remote work was identified as a coping strategy by 16% of respondents, suggesting that those with flexible or digital-based jobs were using it to reduce transport-related expenses. Another 15% reported shifting toward alternative energy sources such as solar power or LPG, pointing to a gradual move by some households and businesses toward alternative energy options during the shortage period.

Only 7% indicated that they had made no adjustments and were continuing with their routines as usual.

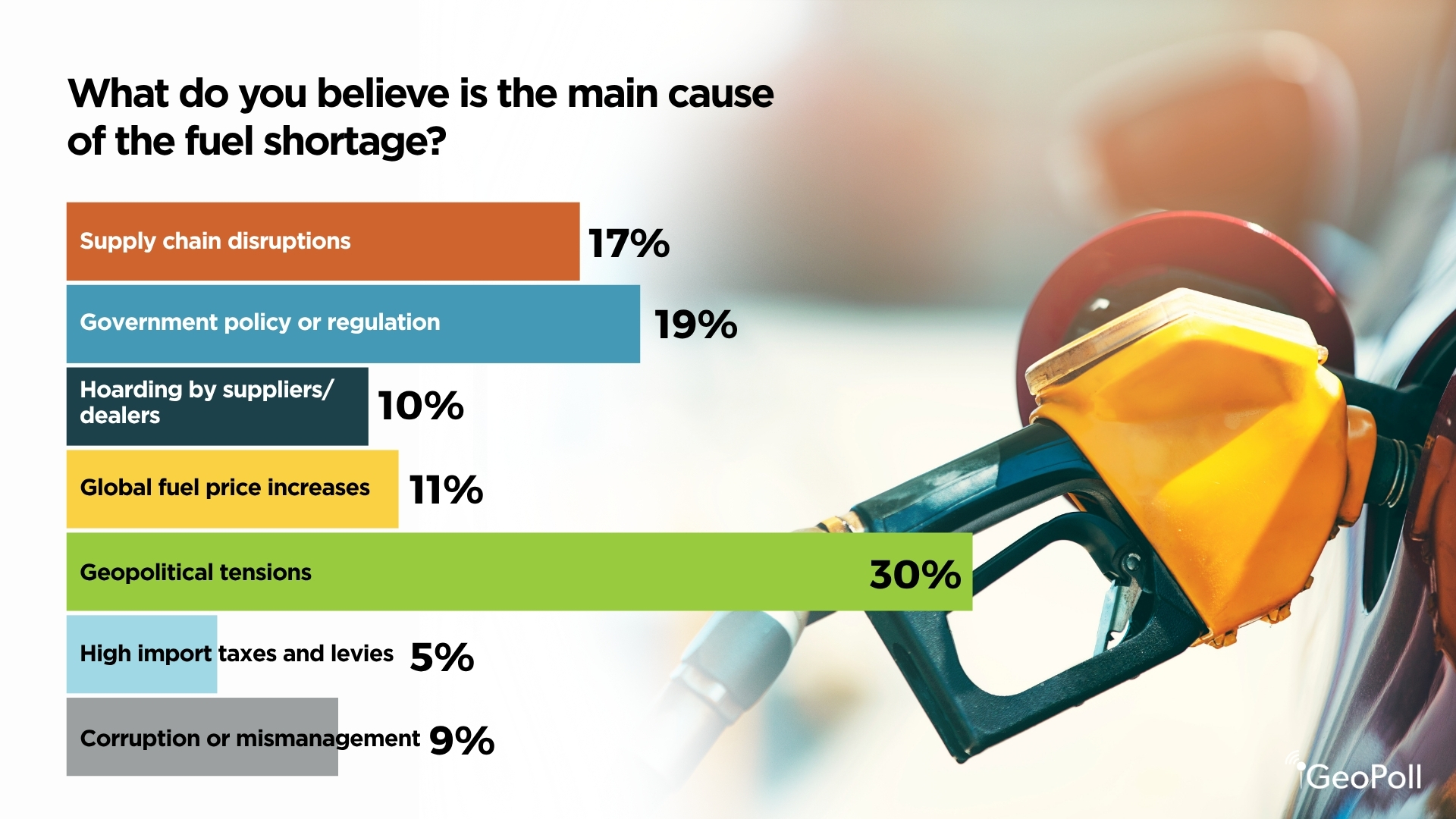

Who, or What, Is to Blame?

Geopolitical tensions were identified as the leading perceived cause of the fuel shortage, cited by 30% of respondents. In particular, many respondents associated the situation with international conflicts and instability affecting global fuel supply and pricing, including tensions involving the United States and Iran. This suggests a strong level of public awareness around the influence of global energy market dynamics on local fuel availability.

At the same time, respondents also pointed to several domestic factors. Government policy and regulation were cited by 19% as the main cause of the shortage, while 17% attributed it to supply chain disruptions. A further 9% blamed hoarding by suppliers and dealers, and another 9% pointed to corruption or mismanagement.

Combined, domestically linked explanations, including policy issues, supply chain challenges, hoarding, corruption, and import-related concerns, accounted for a larger share of responses than geopolitical factors alone, indicating that many respondents viewed the shortage as being driven by both international and local pressures.

Actions taken by the government

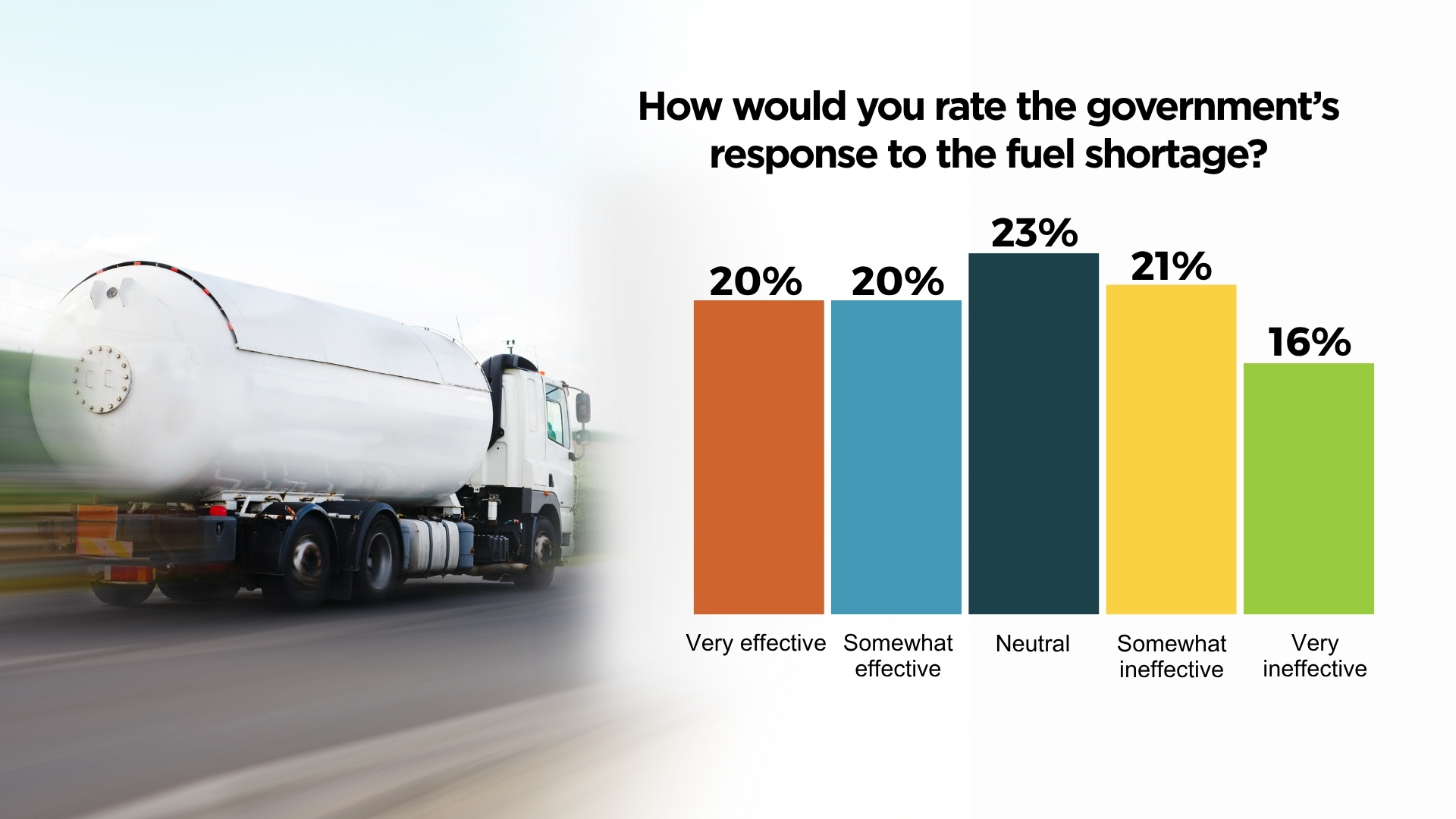

Public opinion on the government’s response to the fuel shortage was divided. A total of 40% of respondents rated the response as effective or very effective, while 37% viewed it as somewhat or very ineffective. Another 23% remained neutral. The relatively even distribution across these views suggests that many respondents were still uncertain about the effectiveness of the response during the survey period. However, the sizeable share expressing dissatisfaction indicates growing concern among a significant portion of the population, particularly given the widespread financial impact of the shortage on households.

What Should Be Done?

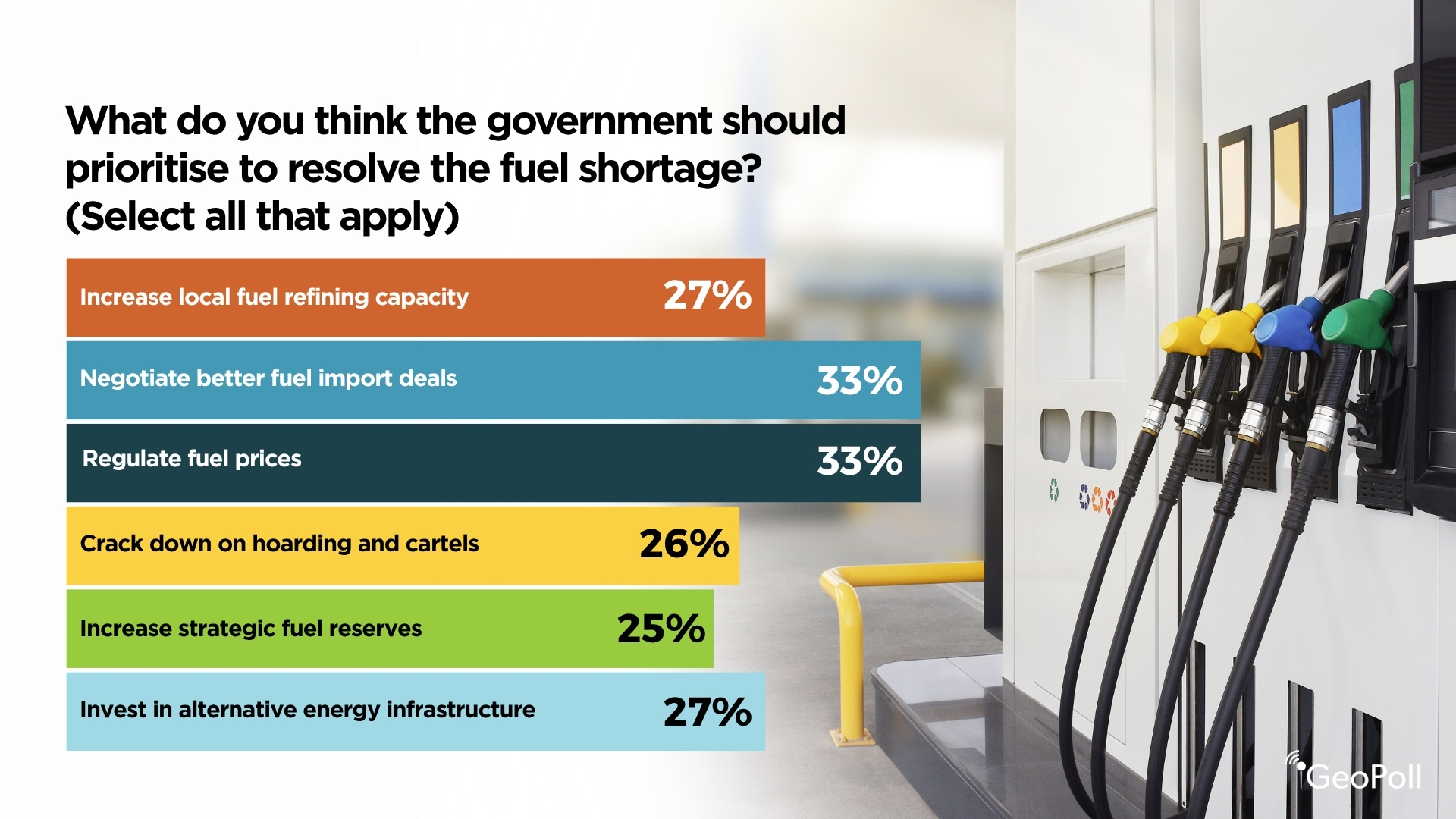

Respondents identified a range of priorities they believed the government should focus on to address the fuel shortage, with no single solution standing out overwhelmingly. Regulating fuel prices and negotiating better import deals were the most cited actions, each selected by 33% of respondents, reflecting strong concern around affordability and fuel supply stability. At the same time, many respondents also supported longer-term measures, including investment in alternative energy infrastructure (27%) and increased local refining capacity (27%). Other priorities included cracking down on hoarding and cartels (26%) and expanding strategic fuel reserves (25%). Overall, the responses suggested that the public was looking for a broad and multi-faceted approach that addresses both the immediate crisis and longer-term energy resilience.

Looking Ahead: No Quick Resolution in Sight

One of the most significant findings from the survey was not only how respondents were experiencing the fuel shortage, but also how long they expected it to continue. Public expectations are important because they influence everyday decisions, from household spending and travel habits to business planning and investment. Respondents generally expressed limited confidence in a quick resolution to the crisis. Only 8% expected the shortage to end within a week, while 14% believed it would be resolved within two weeks. In total, just 22% anticipated a near-term recovery.

By contrast, the majority expected the disruption to continue for a longer period. Twenty-four percent believed the shortage would last about a month, 30% expected it to continue beyond a month, and another 24% viewed it as a potential long-term issue. Combined, 54% of respondents expected the shortage to persist for more than a month or become an ongoing structural challenge. These expectations suggest that many households and businesses may continue adjusting their behaviour in response to prolonged uncertainty, including reducing travel, limiting spending, and slowing economic activity.

Methodology/About this Survey

This Exclusive Survey was powered by GeoPoll’s AI platform; Tuucho run via the GeoPoll mobile application and WhatsApp in Kenya between May 6 and 9, 2026 the sample size was 1,120, composed of random users between 18 and 50. Since the survey was randomly distributed to an and the results are slightly skewed towards younger respondents. All questions were self-administered via mobile survey in English.

The aim of the study was to provide timely, data-driven insights into how the fuel shortage was affecting consumers and businesses, how people were adapting to the disruption, and what they expected in the months ahead. The research also explored public views on the causes of the shortage and perceptions of the government’s response. Through this study, GeoPoll sought to capture real-time public sentiment and contribute actionable insights that can inform policymakers, businesses, development partners, and other stakeholders responding to the crisis.

Please get in touch with us to get more details about our capabilities, explore more on various topics in Africa, Asia, and Latin America.