- Contents

THEMATIC DEEP DIVE: How the Iran–Israel–U.S. Conflict Is Driving a Cost-of-Living Crisis Across the Global South

The Iran–Israel–United States conflict has been reshaping global energy markets since late 2025. For citizens in the Global South, the consequences are neither abstract nor distant. In Pakistan, the government implemented a historic Rs 55 per litre fuel price increase on 6 March 2026. In Kenya, the Energy and Petroleum Regulatory Authority (EPRA) announced on 14 April 2026 the largest fuel price adjustment in over 21 years of regulatory records — a KSh 28.69 per litre increase for petrol and KSh 40.30 for diesel, effective 15 April. In Egypt, subsidised fuel prices were revised upward for the third time in twelve months. In South Africa, the inland price of 95-octane petrol is set to breach some of the highest prices ever seen in the country . These are not coincidences. They are the downstream effects of a single geopolitical shock.

In early March 2026, GeoPoll surveyed 3,754 citizens across Egypt, Kenya, Nigeria, Pakistan, Saudi Arabia, and South Africa as part of our Caught in the Crossfire? citizen perceptions study. Among the study’s most striking findings: the economic dimension of the conflict is being felt acutely and immediately, with fuel prices at the centre of public concern.

| 70% | of respondents across all six countries report that the conflict has affected fuel prices in their country |

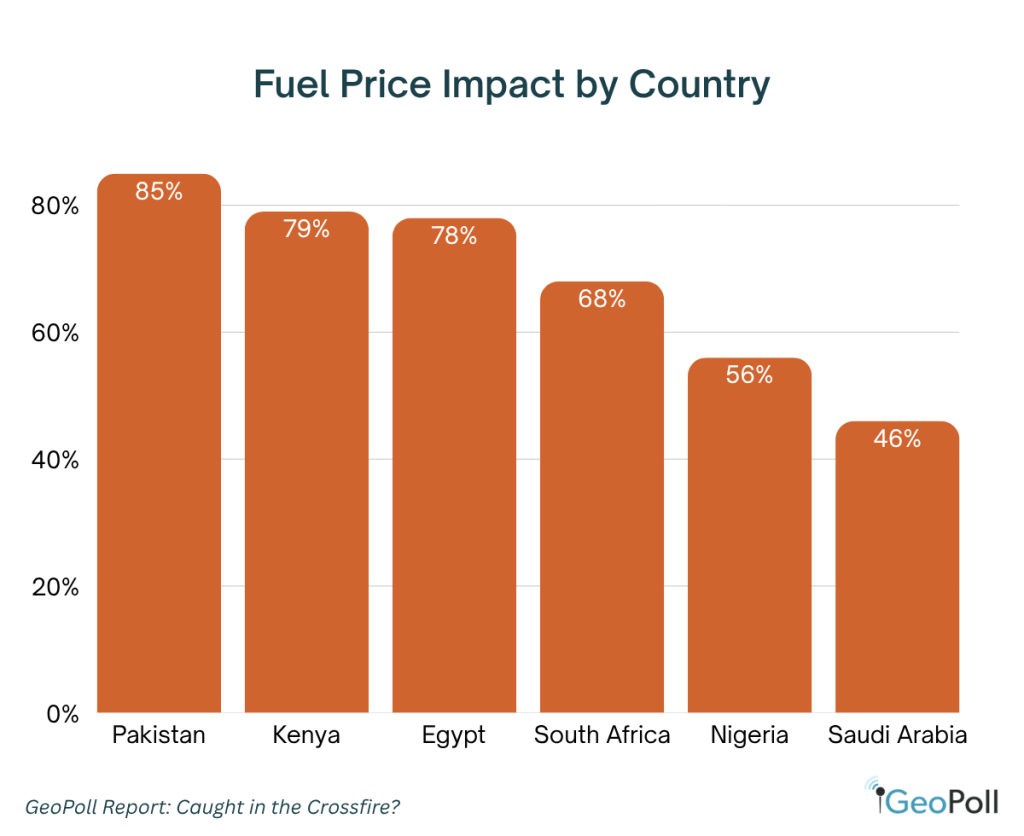

Across the six-country sample, 70% of respondents report that the conflict has affected fuel prices in their country, with 42% characterising the impact as significant. The finding is consistent across diverse economic contexts – from oil-importing economies such as Pakistan and Kenya to the oil-exporting economy of Saudi Arabia, where 46% still report an impact.

The variation across countries reflects both the degree of energy dependence and the extent of government intervention. Pakistan, where the government passed through the full cost of disrupted imports, registers the highest impact at 85%. Saudi Arabia, which benefits from domestic production and price controls, registers the lowest at 46% – though this figure is notable in itself for a major oil producer.

Respondents Reporting or expecting Fuel Price Impact by Country

Country Analysis: The Fuel Crisis on the Ground

Pakistan: The Highest Impact in the Dataset

Pakistan registers the most severe fuel price impact of any country in the study, with 85% of respondents reporting or expecting an effect. The finding is consistent with on-the-ground realities: on 6 March 2026, the government implemented a Rs 55 per litre fuel price increase – among the largest single adjustments in the country’s recent history – directly attributed to rising import costs resulting from conflict-related supply disruptions.

| 85% | of Pakistani respondents report or expect fuel price impact – the highest of any country surveyed |

Fifty percent of Pakistani respondents identify inflation and cost of living as the single most significant economic consequence of the conflict, the highest figure for any country on this measure. Pakistan’s dependence on imported crude oil, combined with a depreciating rupee and constrained foreign exchange reserves, creates a transmission mechanism that converts global oil price shocks directly into consumer-level inflation.

Pakistan also brokered the short-lived ceasefire between Iran and the United States that took effect on 8 April 2026 before collapsing on 12 April. The ceasefire’s failure has further complicated Pakistan’s diplomatic positioning and reinforced public anxiety about prolonged economic disruption.

Kenya: From Shortage to Record-Breaking Price Adjustment

Kenya presents a particularly instructive case study. At the time of surveying in March 2026, Kenya’s fuel prices were government-regulated through the EPRA pricing mechanism, which had effectively absorbed global price increases without passing them to consumers. However, 79% of Kenyan respondents still reported fuel price impact – because the economic strain was manifesting not through prices but through supply disruptions.

By early April, a severe fuel shortage had spread across at least 13 counties. In response, the government deployed KSh 6.2 billion in emergency subsidies and reduced VAT on fuel from 16% to 13%. These measures proved insufficient to contain the crisis.

On 14 April 2026, EPRA announced the largest fuel price adjustment in over 21 years of regulatory records: super petrol now retails at KSh 206.97 per litre in Nairobi, up KSh 28.69 from KSh 178.28, while diesel rises KSh 40.30 to an all-time high of KSh 206.84, effective 15 April. EPRA data indicate that the landed cost of imported super petrol rose 41.5% and diesel 68.7% during the review period. The regulatory body cited “significant increases in the prices of petroleum products in the international market” as the primary driver.

The magnitude of these adjustments points to the unsustainability of shielding consumers from global price shocks through regulation alone, and validates the concerns expressed by the 79% of Kenyan respondents who identified fuel price impact before the price adjustment was officially announced.

| 79% | of Kenyan respondents reported fuel impact even before the record April price hike |

Egypt: Inflation Compounds an Existing Crisis

Seventy-eight percent of Egyptian respondents report fuel price impact. Egypt, which floated its currency in March 2024 and has experienced sustained inflationary pressure, is particularly vulnerable to energy price shocks. The government has raised subsidised fuel prices three times in the past twelve months. Brent crude’s rise from approximately $70 per barrel in late 2025 to over $128 per barrel in March 2026 has placed severe strain on Egypt’s import bill and fiscal position.

Forty-eight percent of Egyptian respondents cite inflation as the most significant economic consequence – the second-highest figure after Pakistan (50%). Nineteen percent identify food prices specifically, the highest of any country, reflecting the compounding effect of energy costs on food production and transport.

South Africa: A Slow-Burning Crisis

Sixty-eight percent of South African respondents report fuel price impact. The inland price of 95-octane petrol exceeded R30 per litre in March 2026. South Africa’s fuel pricing mechanism adjusts monthly based on international crude prices, the rand–dollar exchange rate, and shipping costs – all three of which have moved unfavourably. The Automobile Association of South Africa warned in April that further significant increases are expected for May 2026.

Twenty-two percent of South African respondents cite employment and job losses as the most significant economic consequence – the highest figure for any country on this measure – reflecting broader structural vulnerabilities in an economy already contending with 32% unemployment.

Nigeria: A Producer Still Feeling the Pressure

Despite being Africa’s largest oil producer, 56% of Nigerian respondents report fuel price impact. Nigeria’s Dangote refinery, which began operations in late 2024, has partially insulated the domestic market from global price shocks. However, the naira’s weakness and continued import dependence for refined products mean that global price movements still transmit to consumers, albeit with a lag.

The relatively lower figure compared to other countries in the sample may reflect some insulating effect of domestic production, but 56% still represents a majority reporting impact – a finding that challenges any assumption that oil-producing nations are immune to the conflict’s economic consequences.

Saudi Arabia: Impact Even for the Region’s Largest Producer

Saudi Arabia registers the lowest fuel price impact at 46%, consistent with its position as the world’s largest oil exporter with heavily subsidised domestic fuel prices. That nearly half of Saudi respondents still report an impact suggests the conflict’s economic effects extend beyond fuel pricing to broader cost-of-living increases and market uncertainty.

Inflation is the Primary Economic Consequence

When asked to identify the single most significant economic consequence of the conflict, respondents across all six countries point to inflation and cost of living (43%), followed by fuel prices specifically (27%), food prices (15%), and employment or job losses (13%). The pattern is consistent across countries, though the relative weighting varies with national economic conditions.

| Economic Impact | Pakistan | Egypt | Kenya | S. Africa | Nigeria | Saudi |

| Inflation / CoL | 50% | 48% | 40% | 38% | 35% | 42% |

| Fuel prices | 30% | 22% | 33% | 25% | 30% | 22% |

| Food prices | 10% | 19% | 14% | 12% | 16% | 15% |

| Employment | 8% | 9% | 11% | 22% | 16% | 18% |

The Strait of Hormuz: A Global Chokepoint Under Pressure

The economic dynamics documented in this study are inseparable from developments in the Strait of Hormuz, through which approximately 20% of the world’s daily oil supply transits. Following the collapse of the Pakistan-brokered ceasefire on 12 April 2026, the U.S. Navy intensified its maritime operations in the Persian Gulf, raising the operational risk premium on all crude oil shipped through the strait.

Brent crude prices rose from approximately $70 per barrel in late 2025 to over $128 per barrel by mid-March 2026. While prices have fluctuated with diplomatic developments, the U.S. Energy Information Administration’s revised 2026 forecast of $96 per barrel (up from $74) signals that markets anticipate sustained disruption. For import-dependent economies such as Pakistan, Kenya, and Egypt, each dollar increase in the Brent price translates directly into higher landed costs for fuel, food, fertiliser, and manufactured goods.

Citizen Perspectives

The survey included open-ended responses that contextualise the quantitative findings. The following responses are representative of the concerns expressed across the six-country sample:

| “It’s worrisome as we are in alliance with the States so we could be hit next.”

— Respondent, Pakistan |

| “The price of fuel in South Africa is too high and it has a direct impact on the cost of food and other essential commodities.”

— Respondent, South Africa |

| “The war in the Middle East has made food items and fuel too expensive for the common man.”

— Respondent, Nigeria |

Why This Matters

The data presented in this report demonstrate that the Iran–Israel–U.S. conflict is not merely a geopolitical crisis confined to the Middle East. It is an economic event with measurable, immediate consequences for populations across the Global South. The 70% of respondents reporting fuel price impact, the 92% expressing cost-of-living concern, and the cascading effects on food, transport, and employment represent a humanitarian and policy challenge that extends well beyond the direct conflict zone.

For policymakers, the findings underscore the limits of domestic price controls and subsidies in the face of sustained global energy price shocks. Kenya’s trajectory, from regulated prices to nationwide shortage to record-breaking price adjustment, illustrates the unsustainability of shielding consumers indefinitely from global market forces.

For international organisations and development agencies, the data provide an empirical basis for understanding how distant conflicts translate into lived experience for citizens in Africa, South Asia, and the Middle East. The economic consequences documented here are likely to intensify if the conflict continues or escalates.

Methodology

This report draws on data from GeoPoll’s Caught in the Crossfire? citizen perceptions study, conducted in early March 2026. The study surveyed 3,754 respondents across six countries: Egypt (n = 626), Kenya (n = 627), Nigeria (n = 625), Pakistan (n = 626), Saudi Arabia (n = 624), and South Africa (n = 626).

Respondents were recruited through GeoPoll’s proprietary mobile panel, which uses random sampling from mobile network operator databases to reach nationally representative populations. Surveys were administered via mobile-based interviewing across multiple modes, including CATI, SMS, and mobile web. All respondents were aged 18 and above.

The margin of error for country-level estimates is approximately ±3.9% at a 95% confidence level. Cross-country comparisons should be interpreted with awareness of differing national contexts, including variation in government fuel pricing policies, currency stability, and import dependence.

Access the full 37-page report:

Caught in the Crossfire? A Six-Country Citizen Perceptions Study on the Iran–Israel–U.S. Conflict

For enquiries about country-specific data, custom analysis, or partnership opportunities, contact us.